Add informalnewz.com as a Preferred Source

As a Central recordkeeping Agency of NPS, NSDL CRA appreciates your decision of joining NPS. However, we have noticed that you have not made any contribution in this financial year or the total contribution in your Tier I account for this financial year is less than Rs. 1,000/-. Please contribute at the earliest to avoid freezing of your PRAN XX8811.

You may have witnessed many discussions on various forums discussing which product works best for retirement – NPS or Mutual Funds?

To help you gain clarity we have compared these two very popular retirement investment choices here!

Investment towards a secure and comfortable retirement must largely be based on two golden rules – ‘think long term’ and ‘don’t put all your eggs in one basket’. Staying invested for the longer run not only eliminates the impact of market volatilities but also creates positive returns on the retirement corpus. A balanced and diversified investment typically witnesses lower capital erosions when the markets see a downturn.

Keeping these golden rules in mind and to bring out an effective comparison, NPS Government Sector Scheme – which represents the largest Subscriber base in NPS – is compared with that of Conservative Hybrid Mutual Funds more popularly known as ‘Balanced Funds’.

The basic yardstick of comparison is based on the similarities of investment mix in both the products i.e., 15% exposure to equity and the rest 85% in debt instruments (Government Securities and Corporate Bonds) which is ideal for an investment horizon of more than three years. Another similarity is seen in the frequency of investments – the mandatory monthly contributions of Government employees work similar to those in a Systematic Investment Plan (SIP) of mutual funds.

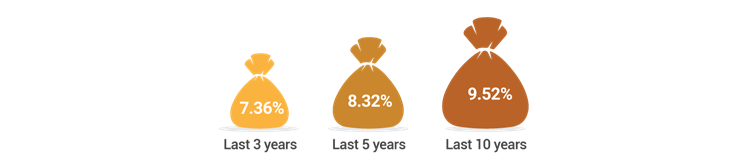

Note: The figures are arrived by taking average of the returns generated by all the three Fund Managers which invest NPS funds of State Govt. employees.

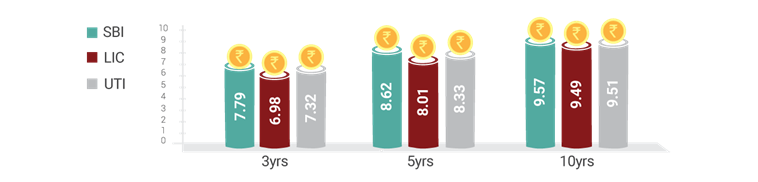

In the NPS Government Scheme, the contributions are invested in three fund managers – SBI, UTI and LIC

Note: The returns are as on 31st March, 2020 evaluating the performance of last 3, 5, and 10 years.

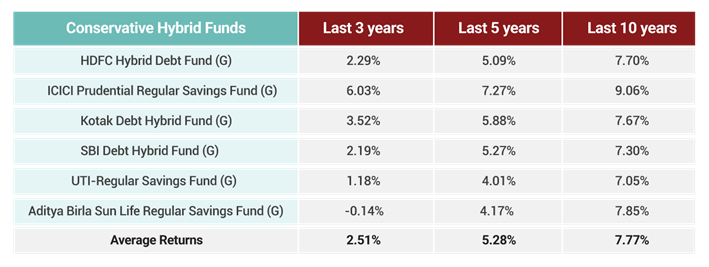

To compare these returns with Mutual Funds, Conservative Hybrid Funds of large fund houses have been shortlisted. The proportion of equity between 20-25% and debt between 75-80% are nearly comparable with that of NPS State Government Scheme.

The comparison clearly reveals that NPS outperforms the average returns generated by the schemes of these popular six fund houses.

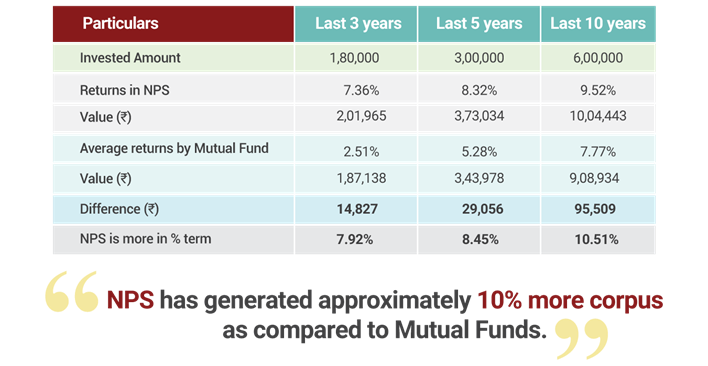

Assumptions: A State Government employee earning ₹25,000 and contributing ₹5,000 (employer + employee contribution) monthly in NPS. This investment is compared with a similar amount invested in hybrid mutual fund.

Despite the assumption that the amount of contribution remains constant, which is unlikely since growth is likely as careers advance, NPS generates more returns than Mutual Funds.

Also, the returns shown here are only for a period of 10 years, while investment towards retirement is done for a period of 30-35 years. Considering the increase in contribution amount over the years as well as a longer investment period, it is safe to say that investment with NPS will create a much larger corpus for a comfortable retirement.

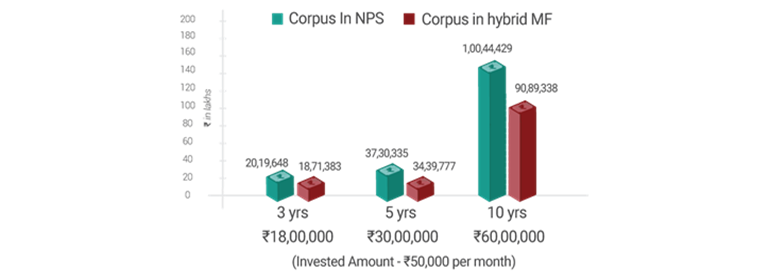

Assuming a higher investment amount of ₹50,000, the returns will be 10 times higher than what it would have been if ₹5,000 is invested per month. The difference in the total corpus will be ₹9,00,000 more than that of Hybrid Mutual Fund.

Government Employees can increase the contribution to NPS by self-contribution over and above the monthly contribution similar to voluntary contribution in EPF, apart from the monthly deduction towards EPF. This additional contribution, will not only increase the adequacy of the retirement corpus, but will also increase the monthly pension in hand.

So, the magnitude of outperformance is higher with a larger investment and over a longer time horizon.

When the investment is for a long period of time, the cost structure or expense ratio plays a substantial role in corpus accumulation. Over a period of 30 to 35 years, the charges can shave off a significant amount from the corpus. The expense ratio of the mutual fund schemes mentioned here are on an average of 1.93%, while the cost structure of NPS is merely 0.17%. This difference can create a substantial dip on the final retirement corpus.

Note: Fees and charges under NPS have been mentioned on NPS Trust website under Charge ratio and Equivalent Asset fee

Assuming that both the products generate the same returns (9%) and the investment is ₹50,000 per year for a period of 10 years, even then, NPS generates ₹85,000 more corpus.

Apart from the considerable benefit of returns and cost on the invested funds, NPS addresses various aspects necessary to create a substantial corpus for retirement. We all know that saving towards retirement is a long term commitment and not a one-time activity. It requires investment discipline and alterations in spending behavior. By nature of the product, NPS helps maintain this discipline and provides flexibility of investment over a long period of time.

So what are you waiting for?

Start investing in NPS from this financial year!